Introduction

In recessions and economic crises, governments introduce monetary and fiscal measures, where banks are encouraged to sanction and enhance the lending and investment facilities to those business entities that are facing liquidity crises. To mitigate the severe negative impact and avoid economic disasters, the governments in the past have adopted heavy domestic and external borrowing. The objectives of such policies were to protect their vote banks, gain popularity, and delay the crisis. Borrowing from commercial banks is one of those strategies adopted over the last several years.

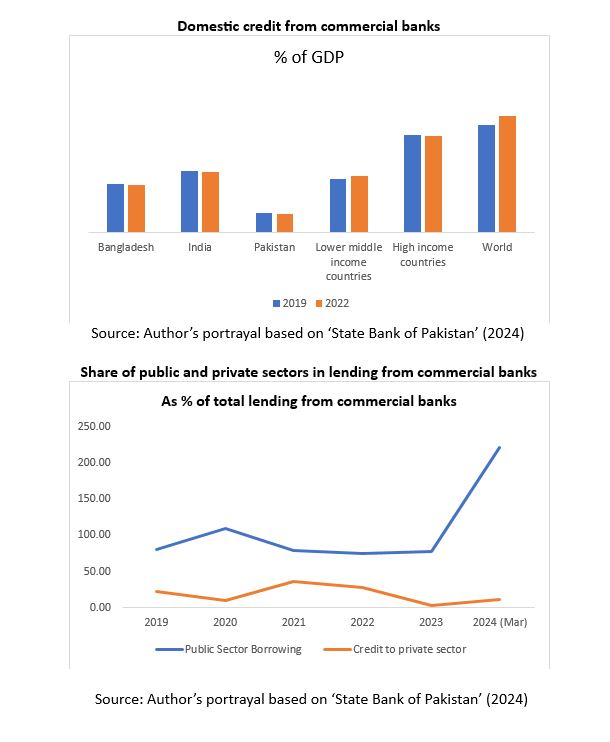

Banks, through their credit policies, can play an important role in alleviating poverty and creating employment opportunities through the creation and enhancement the business opportunities. The world average of domestic credit to the private sector as a percentage of GDP is more than 140%. It is 149% in high-income countries, 140% in upper-middle-income countries, 47% in lower-middle-income countries, and 46% in South Asian countries. The domestic credit as a percentage of GDP in South Asian countries is lower than the rest of the world; the ratio is lowest in Pakistan (excluding Afghanistan). It is 51% in India. However, in Pakistan, it is less than 15 per cent. Since the last decade, there has been a worldwide increasing trend in this ratio; however, it is decreasing in Pakistan year by year.

Public debt in Pakistan

The interconnectedness of the public sector debt, fiscal and monetary policies, and financing for private sector business activities is an important reason for the low domestic credit to the private sector. To protect their vote banks, gain popularity, and delay the onset of a crisis, governments adopt heavy domestic and external borrowing. Borrowing from commercial banks is one of those strategies adopted in Pakistan during the last three decades. From the commercial banks’ point of view, lending to the government is risk-free. But seeing lending to the government as a haven is just an illusion. A government with a high debt-to-GDP ratio and continuous growth in borrowing to repay previous loans seems strange to lenders, and it becomes even stranger if GDP growth is lower than the required growth and the tax base cannot be increased. Oddly enough, the debt liability of the government is ultimately repaid by the private sector through additional taxes or the withdrawal of subsidies or public services. In this situation, lending to the government can be riskier than advances to private businesses, where the earning capacity is visible and assets can be pledged by the lenders.

The domestic credit to the private sector by commercial banks becomes more important in Pakistan because the size of the non-banking financial sector in domestic lending is almost negligible. Almost all of the domestic credit provided to the private sector in Pakistan comes from commercial banks, and the share of the non-banking financial sector is negligible. The huge lending by commercial banks to the government can further affect the volume of domestic credit to the private sector.

Key takeaway

This research identifies that prudential regulations do not discourage lending or investment; rather, it is the monetary and fiscal policies that lead to a decline in credit to the private sector. One of the major important points in this analysis is that almost 100 per cent of domestic credit to the private sector in Pakistan belongs to commercial banks, and the share of the non-banking financial sector is negligible.

By: Dr Ayub Mehar

Professor at Iqra University